CADTH Health Technology Review

Privately Operated Medical Imaging Facilities Across Canada

CMII Service Report

Key Messages

There are at least 85 privately operated facilities in Canada that accept private payment for advanced medical imaging exams (i.e., CT, MRI, single-photon emission computed tomography [SPECT], SPECT and CT [SPECT-CT], and/or positron emission tomography [PET] and CT [PET-CT]).

Quebec has the highest number of private facilities that offer advanced medical imaging exams among provinces, followed by Alberta, British Columbia, and Ontario.

Most private imaging facilities operate in or near census metropolitan areas.

More than half of private imaging facilities operate as part of chain ownerships, and further growth in chain ownership is under way.

Although less than 10% of all CT and MRI exams are delivered in the private setting, they are the most commonly performed type of privately delivered advanced medical imaging exams.

Context

Since the early 2000s, an increase in privately owned imaging facilities has been noted in Canada.1-5 Less than 10% of MRI and CT services were delivered in privately owned imaging facilities in 2018,6 but this may change across all imaging modalities with the planned expansion of private services and chain ownerships and the increase in the acquisition of private facilities by investment firms across Canada.5-8

There is limited information regarding the activities and capacity of privately operated medical imaging facilities in Canada. Data related to privately operated facilities are needed to build a complete and comprehensive picture of advanced medical imaging capacity across the country.

Objective

This report summarizes information on the number and location of privately operated imaging facilities across Canada. The objective of this report is to determine the number and geographic distribution of privately operated medical imaging facilities accepting private payment for advanced medical imaging services, specifically CT, MRI, SPECT, SPECT-CT, and PET-CT. A secondary objective is to identify the number of private medical imaging facilities operating as part of chain ownerships.

Methods

Information on the number of privately owned medical imaging facilities operating advanced imaging equipment was collected for each province (no private imaging facilities operate in the territories9,10). Three primary sources of information were used, including data from previous Canadian Medical Imaging Inventory (CMII) surveys on private imaging,9,10 a web-based directory of Canadian private imaging facilities,11 as well as data sources identified through a Google search. In the few instances when information conflicted between the 3 sources, data from the websites of private imaging facilities were followed because it was assumed to be more up-to-date.

To assess the geographic distribution of privately operated facilities, their location was checked against Statistics Canada’s definition of a census metropolitan area (CMA). A CMA is an area that has a total population of at least 100,000, with 50,000 people or more living within its core.12 Adjacent municipalities must also have a “high degree of integration with the core.”12 Chain ownership of private imaging facilities was also noted when an identified facility operated under the same business name and used the same website domain with at least 1 other medical imaging facility in Canada.

For the purposes of this report, private imaging exams refer to exams billed to payment sources other than provincial health insurance plans (e.g., private insurance, worker compensation boards, or out-of-pocket payments). The term facilities used in this report refers to privately operated medical imaging facilities that accept private payment.

Results

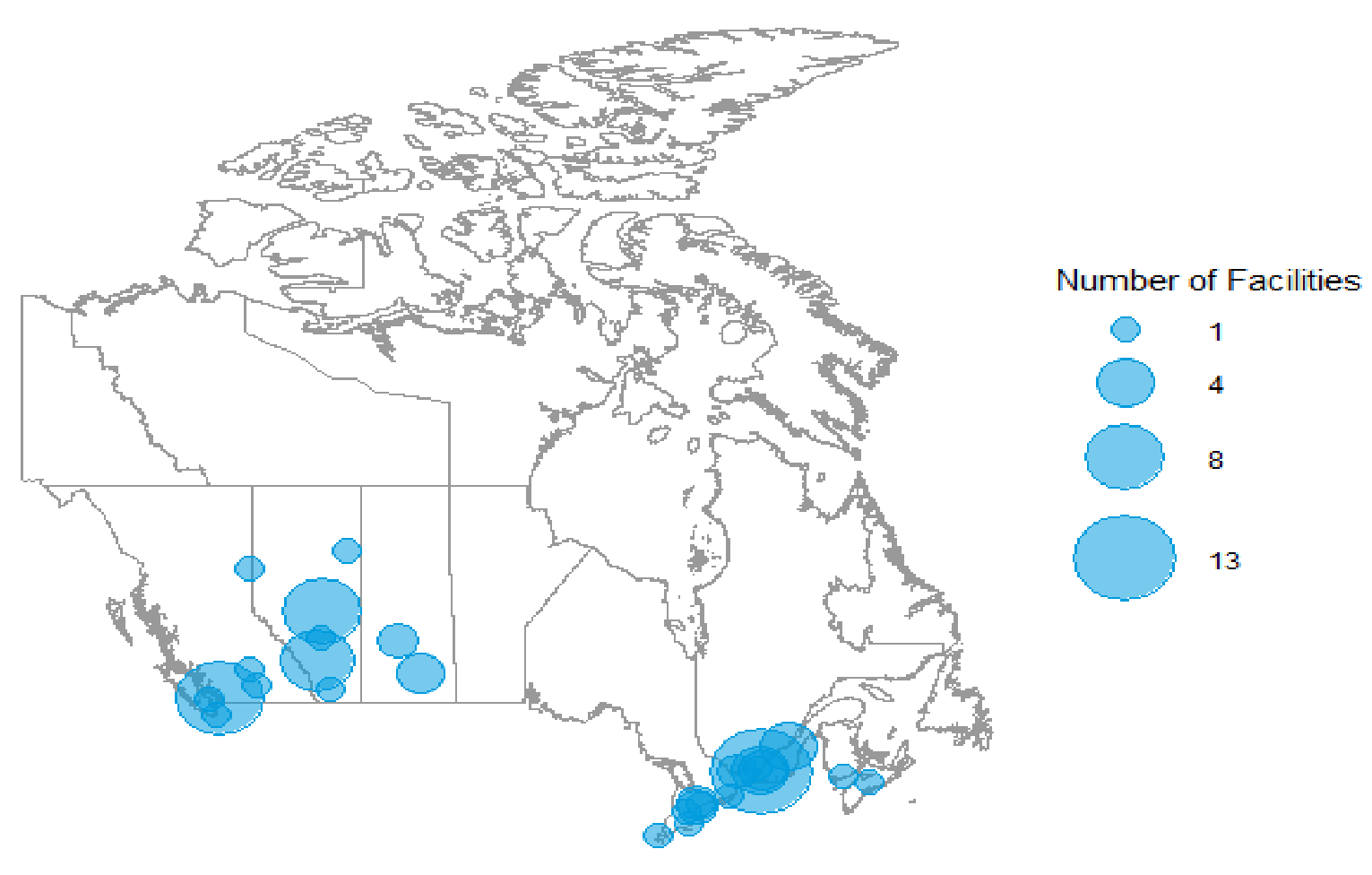

The search identified 85 facilities that offer private MRI, CT, SPECT, SPECT-CT, and PET-CT exams in Canada. Quebec appears to have the most private facilities with 31 of the 85 (36%), followed by Alberta with 18 (21%), British Columbia with 15 (18%), Ontario with 14 (16%), and Saskatchewan with 5 (6%) facilities. In the Atlantic region, there are 2 facilities: 1 in Nova Scotia (1%) and another in New Brunswick (1%).

MRI is the most accessible advanced imaging modality in private facilities across Canada, with 66 (78%) out of the 85 facilities performing these exams, followed by 27 (32%) facilities performing CT exams, 12 (14%) facilities performing SPECT exams, 9 (11%) facilities performing SPECT-CT exams, and 6 (7%) facilities performing PET-CT exams. A summary of provincial private imaging facilities with advanced medical imaging equipment by modality type is presented in Table 1. In many instances, as is the case in the public sector, a single private facility may operate more than 1 type of imaging modality, such as MRI and CT.

Fifty-five (65%) of the 85 facilities are located in CMAs. Most of the facilities located outside of CMAs are within approximately 100 km from a CMA (Figure 1). There are currently no private facilities operating in Manitoba, Newfoundland and Labrador, Prince Edward Island, and the Territories.9,10 Fifty-four (64%) of the 85 facilities operate as part of chain ownerships.

Table 1: Number of Private Facilities With Advanced Medical Imaging Services Across Canada

Province or territory | Total facilities,a n | Facilitiesa offering imaging exams by modality type, n | ||||

|---|---|---|---|---|---|---|

CT | MRI | PET-CT | SPECT | SPECT-CT | ||

Alberta | 18 | 6 | 8 | 0 | 7 | 8 |

British Columbia | 15 | 4 | 14 | 1 | 0 | 0 |

Manitoba | 0 | 0 | 0 | 0 | 0 | 0 |

New Brunswick | 1 | 0 | 1 | 0 | 0 | 0 |

Newfoundland and Labrador | 0 | 0 | 0 | 0 | 0 | 0 |

Northwest Territories | 0 | 0 | 0 | 0 | 0 | 0 |

Nova Scotia | 1 | 0 | 1 | 0 | 0 | 0 |

Nunavut | 0 | 0 | 0 | 0 | 0 | 0 |

Ontario | 14 | 4 | 9 | 3 | 5 | 1 |

Prince Edward Island | 0 | 0 | 0 | 0 | 0 | 0 |

Quebec | 31 | 12 | 29 | 2 | 0 | 0 |

Saskatchewan | 5 | 2 | 4 | 0 | 0 | 0 |

Yukon | 0 | 0 | 0 | 0 | 0 | 0 |

Canada | 85 | 27 | 66 | 6 | 12 | 9 |

aFacilities refers to privately operated medical imaging facilities that accept private payment.

Figure 1: Locations of Private Facilities Across Provinces and Territories With Advanced Medical Imaging Services

Note: This map was created using 2021 census cartographic files from Statistics Canada.13

Alberta

There are at least 18 private imaging facilities operating in Alberta. Of the 18 facilities identified, 8 (44%) provide MRI exams, 6 (33%) provide CT exams, 7 (39%) provide SPECT exams, and 8 (44%) provide SPECT-CT exams. Fifteen of the 18 (83%) private facilities are in Alberta’s most populated metropolitan areas: Edmonton, Calgary, Lethbridge, and Red Deer,14 which are CMAs.14 Two additional facilities operate in urban areas adjacent to Edmonton, Spruce Grove, and Sherwood Park, and 1 facility is in Fort McMurray in northeast Alberta. Of these 18 private facilities, 17 operate as part of chain ownerships.

British Columbia

There are at least 15 private imaging facilities operating in British Columbia. Fourteen of the 15 (93%) facilities identified provide MRI exams, 4 (27%) facilities provide CT exams, and 1 (7%) facility provides PET-CT exams. Of the 15 facilities, 8 (53%) operate in CMAs: 4 in Vancouver, 1 in Kamloops, 1 in Kelowna, 1 in Victoria, and 1 in Nanaimo.14 The remaining 7 facilities are not in CMAs; 2 operate in Surrey and there is 1 facility in each of the following 5 locations: Burnaby, Coquitlam, Dawson Creek, North Vancouver, and Richmond. Five of the 15 private facilities operate as part of chain ownerships.

Saskatchewan

There are at least 5 private imaging facilities in Saskatchewan. All 5 facilities identified provide MRI exams, and 2 (40%) facilities provide CT exams. Two (40%) facilities are located in Saskatoon and 3 (60%) are in Regina, both cities are CMAs.14 Four of the 5 private facilities operate as part of 2 chain ownerships.

Ontario

There are at least 14 private imaging facilities in Ontario. Of the 14 facilities identified, 9 (64%) provide MRI exams, 4 (29%) provide CT exams, 5 (36%) provide SPECT exams, 1 (7%) provides SPECT-CT exams, and 3 (21%) provide PET-CT exams. One private facility is located within a publicly operated hospital in a CMA.9 Eleven (79%) facilities are in the greater Toronto area, including 2 in the Toronto CMA. The remaining 3 private facilities are in the CMAs of Windsor, Kitchener, and Kingston.14 Nine of the 14 private facilities operate as part of chain ownerships.

In early 2023, Ontario announced a plan to expand diagnostic and surgical procedures to private facilities and introduce legislation to allow private facilities to conduct more CT and MRI scans.8 This may prompt an increase in the number of privately operated facilities in Ontario. A company with many facilities across North America plans to open a location in Toronto in 2023.15

Quebec

There are at least 31 private imaging facilities in Quebec. Among the 31 private facilities identified, all provide MRI exams, 12 (39%) provide CT exams, and 2 (6%) provide PET-CT exams. The Montreal CMA has the largest proportion of Quebec’s private facilities with 13 (42%) of the 31 facilities.14 Another 7 of the 31 facilities are also in CMAs, specifically 4 (13%) in Quebec City, 2 (6%) in Gatineau, and 1 (3%) in Le Saguenay.14 The remaining 11 (35%) facilities are in areas not considered a CMA by Statistics Canada.14 Of the 11 facilities, 4 are in Laval, 3 in Longueuil, and there are 1 each in Roussillon, Francheville, Les Moulins, and Sainte-Thérèse. Nineteen of the 31 private facilities operate as part of chain ownerships.

New Brunswick

At least 1 private imaging facility offers MRI services in Moncton, an area considered to be a CMA.14 No other advanced imaging modalities operating in the private setting were identified in this province.

Nova Scotia

At least 1 private facility offers MRI services in Halifax, an area considered to be a CMA.14 No other advanced imaging modalities operating in the private setting were identified in this province.

Limitations

Information on private imaging facilities was consolidated from information available on the websites of private imaging facilities and from previous CMII surveys. The most recent CMII survey was completed in 2020; therefore, some of the data collected for this report may be out of date.

For many private facility websites, “nuclear medicine exams” were reported as available but the specific imaging modality was not specified. Nuclear medicine is inclusive of planar scintigraphy in addition to SPECT, SPECT-CT, and PET-CT.16 Given the cost of PET-CT equipment, and its relative obscurity to other nuclear imaging modalities, it was assumed that if it was not specifically mentioned on the websites of private imaging facilities then it was not available.17,18 Similarly, SPECT and SPECT-CT were only considered if the facility website explicitly stated availability or if the CMII database indicated their presence at the facility.

The actual number of imaging equipment at each facility was not readily available from most websites. For example, if a facility reported MRI availability, it was assumed that there was 1 MRI unit rather than multiple units.

This report considered facilities that offer MRI, CT, SPECT, SPECT-CT, and/or PET-CT. Facilities that solely offered medical imaging exams that were outside the scope of this report, such as X-ray or ultrasound, were not considered for inclusion.

Conclusion

There are at least 85 advanced medical imaging facilities that accept payment from private sources in Canada. MRI exams are the most commonly performed advanced medical imaging service at these facilities followed by CT. Exams conducted with SPECT, SPECT-CT, and PET-CT are less commonly performed in private facilities in Canada. Among the provinces, Quebec, followed by Alberta, British Columbia, and Ontario, operates most of Canada’s facilities that accept private payment. No record of such facilities in Manitoba, Newfoundland and Labrador, Prince Edward Island, and the Territories were identified.

The private imaging landscape is anticipated to change in Canada as the use of private services, investment firm ownership (those financed by private equity), and independent for-profit chain ownership continues to increase.

References

1.Allin S, Sherar M, Church Carson M, Jamieson M, et al. Public management and regulation of contracted health services. A rapid review prepared for the Institute for Health Economics (Rapid review No 23). Toronto (ON): North American Observatory on Health Systems and Policies; 2020: https://ihpme.utoronto.ca/wp-content/uploads/2020/02/NAO-Rapid-Review-23_EN.pdf. Accessed 2022 Dec 5.

2.Tiedemann M. The Canada health act: an overview. (Background paper; publication no. 2019-54-E). Ottawa (ON): Library of Parliament; 2019 Dec 17: https://lop.parl.ca/staticfiles/PublicWebsite/Home/ResearchPublications/BackgroundPapers/PDF/2019-54-e.pdf. Accessed 2022 Dec 5.

3.Ontario Health Coalition. Private clinics and the threat to public medicare in Canada: results of surveys with private clinics and patients. Ottawa (ON): Ontario Health Coalition; 2017: https://www.healthcoalition.ca/wp-content/uploads/2017/06/Private-Clinics-Report.pdf. Accessed 2022 Dec 5.

4.Novacap Managment Inc. Canada diagnostic centres and Novacap partner to accelerate the national expansion of one of Canada's largest medical imaging groups. 2021; https://www.prnewswire.com/news-releases/canada-diagnostic-centres-and-novacap-partner-to-accelerate-the-national-expansion-of-one-of-canadas-largest-medical-imaging-groups-301325757.html. Accessed 2022 Dec 5.

5.DeRosa K. Private medical services getting B.C. government cash despite extra-billing allegations: report. Vancouver Sun. 2022 Aug 24. https://vancouversun.com/news/local-news/private-medical-services-getting-government-cash-despite-extra-billing-allegations-report. Accessed 2022 Dec 5.

6.Valand HA, Chu S, Bhala R, Foley R, Hirsch JA, Tu RK. Comparison of advanced imaging resources, radiology workforce, and payment methodologies between the United States and Canada. AJNR American journal of neuroradiology. 2018;39(10):1785-1790. PubMed

7.Government of Saskatchewan. Saskatchewan introduced new legislation to license user-pay MRI services. 2015; https://www.saskatchewan.ca/government/news-and-media/2015/may/06/mri-legislation. Accessed 2022 Dec 5.

8.Ontario Government. Ontario reducing wait times for surgeries and procedures. 2023; https://news.ontario.ca/en/release/1002641/ontario-reducing-wait-times-for-surgeries-and-procedures. Accessed 2022 Dec 5.

9.Chao YS, Sinclair A, Morrison A, Hafizi D, Pyke L. The Canadian medical imaging inventory 2019-2020. (CADTH health technology review). Can J Health Technol. 2021;1(1):1-215. https://cadth.ca/sites/default/files/ou-tr/op0546-cmii3-final-report.pdf. Accessed 2022 Dec 5.

10.Santos C. Private imaging facilities in Canada: MRI and CT. (Canadian medical imaging inventory). Ottawa (ON): CADTH; 2022: https://www.cadth.ca/sites/default/files/attachments/2022-06/CMII-MRI-CT-Final_3.pdf. Accessed 2022 Dec 5.

11.Findprivateclinics.ca. https://www.findprivateclinics.ca/. Accessed 2022 Dec 5.

12.Statistics Canada. Census metropolitan area (CMA) and census agglomeration (CA). (Dictionary, census of population, 2021) 2021 Nov 17 (updated 2022 Feb 9); https://www12.statcan.gc.ca/census-recensement/2021/ref/dict/az/Definition-eng.cfm?ID=geo009. Accessed 2022 Dec 5.

13.Statistics Canada. 2021 Census - boundary files. 2021; https://www12.statcan.gc.ca/census-recensement/2021/geo/sip-pis/boundary-limites/index2021-eng.cfm?year=21. Accessed 2022 Dec 5.

14.Statistics Canada. Table 2: Population and population growth rate of census metropolitan areas in Canada, 2011 to 2016 and 2016 to 2021 ranked by percentage of growth in 2021. (The Daily) 2022; https://www150.statcan.gc.ca/n1/daily-quotidien/220209/t002a-eng.htm. Accessed 2022 Dec 5.

15.Prenuvo. Our locations. 2022; https://prenuvo.com/locations/. Accessed 2022 Dec 5.

16.Wang Y. Nuclide imaging: planar scintigraphy, SPECT, PET. [2013]; https://eeweb.engineering.nyu.edu/~yao/EL5823/NuclearImaging_ch8_9.pdf. Accessed 2022 Dec 5.

17.Jones T, Townsend D. History and future technical innovation in positron emission tomography. J Med Imag (Bellingham, Wash). 2017;4(1):011013-011013. PubMed

18.Vu T, Santos C. The implementation considerations of PET-CT. (Canadian medical imaging inventory service report). Ottawa (ON): CADTH; 2022: https://www.cadth.ca/sites/default/files/attachments/2022-01/implementation_considerations_of_PET-CT.pdf. Accessed 2022 Dec 5.

ISSN: 2563-6596

Disclaimer: The information in this document is intended to help Canadian health care decision-makers, health care professionals, health systems leaders, and policy-makers make well-informed decisions and thereby improve the quality of health care services. While patients and others may access this document, the document is made available for informational purposes only and no representations or warranties are made with respect to its fitness for any particular purpose. The information in this document should not be used as a substitute for professional medical advice or as a substitute for the application of clinical judgment in respect of the care of a particular patient or other professional judgment in any decision-making process. The Canadian Agency for Drugs and Technologies in Health (CADTH) does not endorse any information, drugs, therapies, treatments, products, processes, or services.

While care has been taken to ensure that the information prepared by CADTH in this document is accurate, complete, and up-to-date as at the applicable date the material was first published by CADTH, CADTH does not make any guarantees to that effect. CADTH does not guarantee and is not responsible for the quality, currency, propriety, accuracy, or reasonableness of any statements, information, or conclusions contained in any third-party materials used in preparing this document. The views and opinions of third parties published in this document do not necessarily state or reflect those of CADTH.

CADTH is not responsible for any errors, omissions, injury, loss, or damage arising from or relating to the use (or misuse) of any information, statements, or conclusions contained in or implied by the contents of this document or any of the source materials.

This document may contain links to third-party websites. CADTH does not have control over the content of such sites. Use of third-party sites is governed by the third-party website owners’ own terms and conditions set out for such sites. CADTH does not make any guarantee with respect to any information contained on such third-party sites and CADTH is not responsible for any injury, loss, or damage suffered as a result of using such third-party sites. CADTH has no responsibility for the collection, use, and disclosure of personal information by third-party sites.

Subject to the aforementioned limitations, the views expressed herein are those of CADTH and do not necessarily represent the views of Canada’s federal, provincial, or territorial governments or any third-party supplier of information.

This document is prepared and intended for use in the context of the Canadian health care system. The use of this document outside of Canada is done so at the user’s own risk.

This disclaimer and any questions or matters of any nature arising from or relating to the content or use (or misuse) of this document will be governed by and interpreted in accordance with the laws of the Province of Ontario and the laws of Canada applicable therein, and all proceedings shall be subject to the exclusive jurisdiction of the courts of the Province of Ontario, Canada.

The copyright and other intellectual property rights in this document are owned by CADTH and its licensors. These rights are protected by the Canadian Copyright Act and other national and international laws and agreements. Users are permitted to make copies of this document for non-commercial purposes only, provided it is not modified when reproduced and appropriate credit is given to CADTH and its licensors.

About CADTH: CADTH is an independent, not-for-profit organization responsible for providing Canada’s health care decision-makers with objective evidence to help make informed decisions about the optimal use of drugs, medical devices, diagnostics, and procedures in our health care system.

Funding: CADTH receives funding from Canada’s federal, provincial, and territorial governments, with the exception of Quebec.

Questions or requests for information about this report can be directed to Requests@CADTH.ca